THE RISE OF THE LONGEVITY FAMILY OFFICE

- Longevity Investors

- Apr 24

- 7 min read

Private capital isn't just funding the science of longer life. It's building the economy around it.

Something has shifted in how the world's most sophisticated private capital thinks about longevity. The question is no longer whether to allocate. It is how much, through which structure, and how fast to move before the window narrows.

The macro context is now well-established. UBS projected in March 2025 that the global longevity market will grow from $5.3 trillion in 2023 to $8 trillion by 2030 - surpassing AI as the world's largest emerging investment category. Global longevity investment more than doubled in a single year, from $3.82 billion in 2023 to $8.49 billion across 331 deals in 2024, according to Longevity.Technology's Annual Investment Report. At Davos 2026, the World Economic Forum dedicated a session to the question "Can We Afford Longevity?" - with centenarians set to quadruple by 2056, healthy ageing has moved from wellness conversation to economic policy priority.

That is the backdrop. What is happening inside private capital is more specific - and more instructive.

Where the Conviction Capital Has Gone

The clearest signal of category maturation is where the largest and most disciplined private allocators have placed their bets.

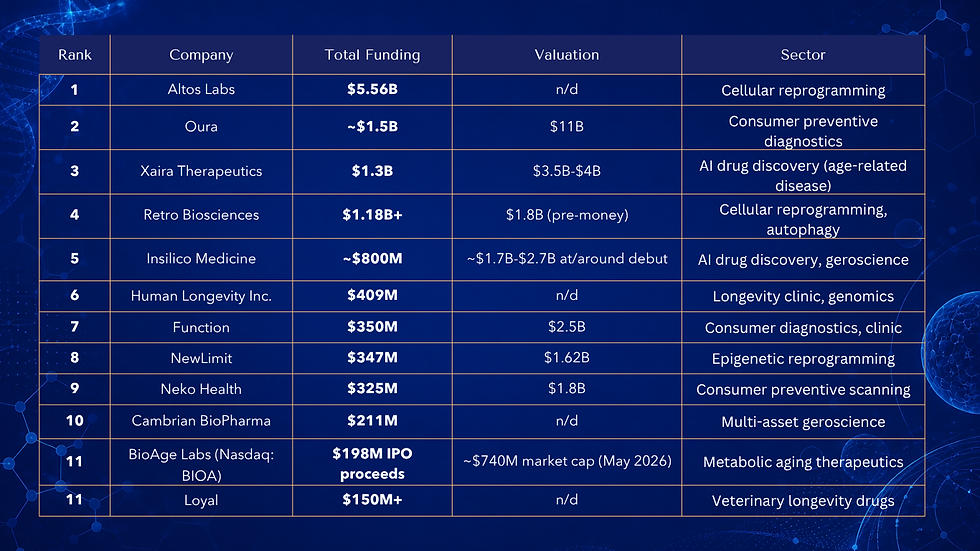

Jeff Bezos anchored Altos Labs at $3 billion in 2022 - still the largest single longevity raise in history - backing cellular reprogramming science aimed at reversing biological aging. Sam Altman personally committed $180 million to Retro Biosciences, then went further: in August 2025, Retro and OpenAI announced a partnership that made cellular reprogramming 50 times more efficient, with human trials of RTR-242 already underway. Coinbase co-founder Brian Armstrong co-founded NewLimit, which raised $130 million in 2025 on a $5 billion valuation. Peter Thiel has backed both the Methuselah Foundation and Unity Biotechnology. Larry Ellison has invested in Life Biosciences and Human Longevity Inc. The Chan Zuckerberg Initiative has committed billions toward understanding and defeating disease at the cellular level, with aging biology central to its research agenda. Yuri Milner co-anchored Altos Labs alongside Bezos. Sector-wide biopharma M&A exceeded $65 billion through October 2025 as large pharma accelerated its acquisition of longevity pipelines.

Seven of the world's most financially disciplined capital allocators have independently made large, long-dated bets on the same category. That pattern carries information that no analyst report quite captures.

The consumer and diagnostics layer is equally telling. Function Health raised $298 million in a Series B - the largest disclosed private round in consumer longevity. Neko Health, Viome, Tally Health, and Acorn Biolabs collectively raised over $700 million alongside it. OURA raised $200 million in a Series D. Insilico Medicine raised $110 million in 2025 for an AI drug discovery platform with 20-plus preclinical candidates already in development. Longevity funding has moved decisively beyond drug pipelines.

Why Family Offices Are the Most Important New Entrant

The Campden Wealth / RBC North America Family Office Report 2025, covering 317 offices managing a collective $554 billion in net wealth, confirms that private markets now account for 29% of the average family office portfolio- the single largest asset class. Nearly half of participating offices expect generational wealth transfer within the next decade. These are institutions built for 50-to-100-year time horizons.

That architecture is precisely what longevity investing demands. Cellular reprogramming, clinical infrastructure, and precision diagnostics platforms are not three-to-five year positions. They require patient, illiquid capital that institutional mandates almost never permit - but that family offices are structurally designed to deploy.

The LIC 2025 investor intelligence data makes the shift concrete. Among the most active investors in the longevity community: 80% of deployed longevity capital sits in private markets. Over 85% are already in active positions. The typical allocator has built 15 to 20 investments over 3 to 4 years.

Fifteen to twenty positions over three to four years is not thematic exposure. It is deliberate category construction - the kind of systematic allocation family offices reserve for private equity or real estate. These investors have crossed a threshold. Longevity is a core allocation, not a satellite bet.

The personal dimension matters too. The principals writing these cheques are often in their 50s and 60s. They are potential beneficiaries of the science they fund. The alignment between financial return and personal mission creates a depth of conviction - and a willingness to hold through difficulty - that is qualitatively different from any other position in a family office portfolio.

![[GRAPHIC 3] This is what conviction capital looks like in longevity. LIC 2025 investor intelligence shows a community that has moved well past exploration - building structured, multi-position portfolios with the same deliberation normally reserved for private equity or real estate.](https://static.wixstatic.com/media/d7bd09_193856e8383e41cfb71725a32242a386~mv2.png/v1/fill/w_980,h_551,al_c,q_90,usm_0.66_1.00_0.01,enc_avif,quality_auto/d7bd09_193856e8383e41cfb71725a32242a386~mv2.png)

Five Places the Capital Is Flowing

The LIC 2025 data reveals five distinct patterns in how active family office capital is being deployed.

1. Longevity biotech and deep science. Altos Labs, Retro Biosciences, NewLimit, Rubedo Life Sciences, Insilico Medicine. The most asymmetric returns, the longest development timelines. The regulatory environment is beginning to move: the FDA rewrote drug approval rules in February 2026 to allow single pivotal trial pathways, and Loyal's LOY-002 secured FDA efficacy acceptance as the first longevity drug in veterinary medicine - establishing that longevity endpoints are legitimate regulatory targets for the first time.

2. AI and precision diagnostics. Function Health, Neko Health, Insilico Medicine, Viome. The data asset being built by longitudinal biomarker platforms compounds in value as patient datasets grow. Retro and OpenAI's reprogramming partnership is the clearest signal yet that the most capable AI in the world is now being pointed directly at aging biology.

3. Longevity clinics and B2B health services - a segment that has matured faster than almost anyone predicted. Canyon Ranch, Lanserhof, SHA Wellness, Chenot Palace, Six Senses, and Four Seasons are all deploying clinical longevity programming at scale. Clinique La Prairie in Montreux has become the anchor clinical partner for The Estate, the new longevity hospitality brand co-founded by Sam Nazarian and Tony Robbins, with $35,000-per-year clinic memberships and planned openings in Miami, London, and the Gulf. Longevity clinics are no longer boutique. They are a replicable B2B model.

4. Real estate and longevity convergence. The Global Wellness Summit named longevity residences a top 2026 investment trend. The hotel market serving the over-60 demographic is projected to grow from $259 billion in 2023 to $412 billion by 2030. Combined longevity-adjacent hospitality totalled $786 billion in 2023, heading toward $1.2 trillion by 2030. Properties integrating diagnostics, concierge medicine, and longevity programming generate yield today while appreciating as the ecosystem matures around them.

5. Geographic expansion strategy. The US still accounts for 84% of total longevity deal volume and 57% of longevity companies globally. But Switzerland, the UK, and Finland are emerging as European hubs. The Gulf is accelerating. The most thoughtful family offices are building geographic diversification into their longevity portfolios - not just for regulatory optionality, but because the longevity economy will be built across multiple jurisdictions simultaneously.

The Infrastructure Thesis

There is a distinction that separates the most sophisticated longevity family offices from everyone else. They are not picking companies. They are building infrastructure.

A position in a diagnostics platform, combined with equity in a clinics network, combined with a deep science bet on cellular reprogramming, is not a diversified portfolio. It is a vertically integrated thesis about what the longevity economy looks like at scale. Annual US healthcare expenditure reached $4.9 trillion in 2023 - with 85% directed at chronic disease management rather than prevention. The entire existing system is built to manage decline. The longevity economy is being built to prevent it. The gap between those two models is the investment opportunity of this generation.

The family offices that understand this are not waiting for the science to de-risk, for regulation to clarify, or for mainstream validation to arrive. They are building positions now - across multiple layers, with the understanding that the category will be defined before the institutional world catches up.

The investors building that architecture gather each September in Gstaad at the Longevity Investors Conference - the most concentrated private gathering of this community in the world. That conversation is deepening. The capital behind it is not slowing down.

References

[1] UBS Chief Investment Office. Investing in Longevity - Transformational Innovation Opportunity. March 28, 2025. https://www.ubs.com/global/en/wealthmanagement/insights/marketnews/article.2048635.html

[2] Longevity.Technology. 2024 Annual Longevity Investment Report. May 13, 2025. https://longevity.technology/investment/report/annual-longevity-investment-report-2024/

[3] World Economic Forum Annual Meeting 2026. Can We Afford Longevity? January 2026. https://www.weforum.org/meetings/world-economic-forum-annual-meeting-2026/sessions/can-we-afford-longevity/

[4] Campden Wealth / RBC. The North America Family Office Report 2025. October 16, 2025. https://www.campdenwealth.com/report/north-america-family-office-report-2025

[5] TechCrunch. Retro Biosciences, backed by Sam Altman, is raising $1 billion to extend human lifespan. January 24, 2025. https://techcrunch.com/2025/01/24/retro-biosciences-backed-by-sam-altman-is-raising-1-billion-to-extend-human-lifespan/

[6] Crunchbase News. Longevity Startup Funding Sees Fewer Moonshots, But Plenty of Buzzy Investments. November 2025. https://news.crunchbase.com/venture/longevity-startup-funding-2025-newlimit-data/

[7] New Market Pitch. Top Longevity Startups by Fundraising 2026. https://newmarketpitch.com/blogs/news/longevity-top-startups-fundraising

[8] New Market Pitch. Longevity Market Funding Trends 2022-2026. https://newmarketpitch.com/blogs/news/longevity-funding-trends

[9] Longevity.Technology. FDA Rewrites Drug Approval Rules and Longevity Stands to Gain. February 2026. https://longevity.technology/news/fda-rewrites-drug-approval-rules-and-longevity-stands-to-gain/

[10] Hospitalitynet / Mogelonsky. The Estate Hotels and Residences Heralds a New Era for Longevity Tourism. December 2025. https://www.hospitalitynet.org/opinion/4124953.html

[11] Senior Trade / Global Wellness Summit. Healthspan Hits Home: Longevity Residences Named a Top 2026 Trend. January 2026. https://www.seniortrade.com/post/healthspan-hits-home-global-wellness-summit-names-longevity-residences-a-top-2026-trend

[12] Seveno Capital. What is Longevity? November 2025. https://seveno.capital/seveno-capital-backs-the-well-estate-2/

[13] LIC 2025 Investor Intelligence Data. Longevity Investors Conference, Gstaad, Switzerland.

Comments